During the past weeks, a series of events and reactions revolving around Bank Al Maghrib’s decision to further increase policy rate by 50 bps to 3% provided the ongoing inflation debate with another pulse of traction. This article aims to take stock of the different views expressed and to lay out explanatory frameworks to envision how Morocco will grapple with inflation over the different horizons.

Cooling yet uncertain global outlook, a heated local context:

While shockwaves stemming from supply-demand mismatches of the post-Covid era and from the inflationary impact of Russia-Ukraine conflict on commodities markets are dampening at the global level, inflation debate is heating in Morocco as the holy month of Ramadan further projected the spotlight on price levels, especially food & beverages.

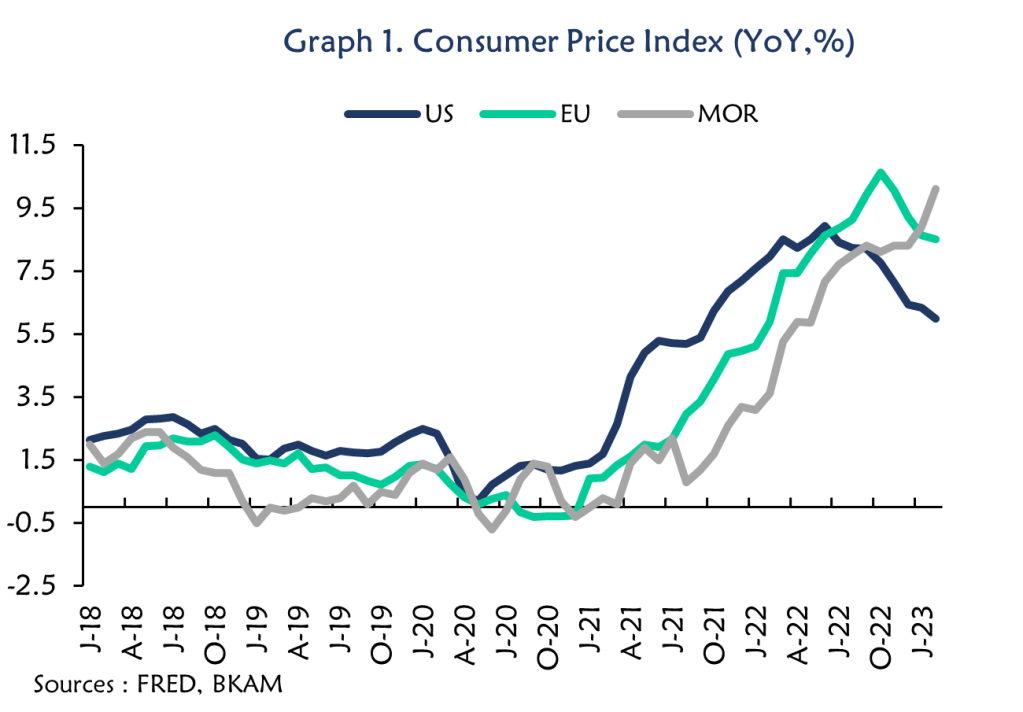

Global inflation outlook is still highly uncertain as recent financial fragilities have motivated many observers to call for a slow-down of the rate hike cycle. OPEC+ recent cuts decision signals the functioning of main central banks anti-inflationary measures, even though it also points to their reversibility. What is in turn certain is the steady and significant progression of price levels in Morocco. Headline CPI printed at 10.1% YoY in Feb. 2023, a 40-years high, while core inflation was reported at 8.5% YoY, with a 0.8% progression MoM. Food items were main contributors in these record-breaking figures, with a YoY growth of 20.1%.

However, despite the alarming last local inflation data, observers still tend to agree on the resilience of Morocco’s inflation cycle’s convergence with those of its main European trading partners.

The point of contention : the nature of inflation

Much of the debate erupted following Ahmed Lahlimi, the Haut Commissariat au Plan chief (the country’s national statiscal office), shared with press his view on the inadequacy of monetary tools to adress Morocco’s inflationary woes. The underlying analysis behind Lahlimi’s statement is that current inflation dynamics in Morocco are far from being driven by supply shocks/lags or demand overheat.

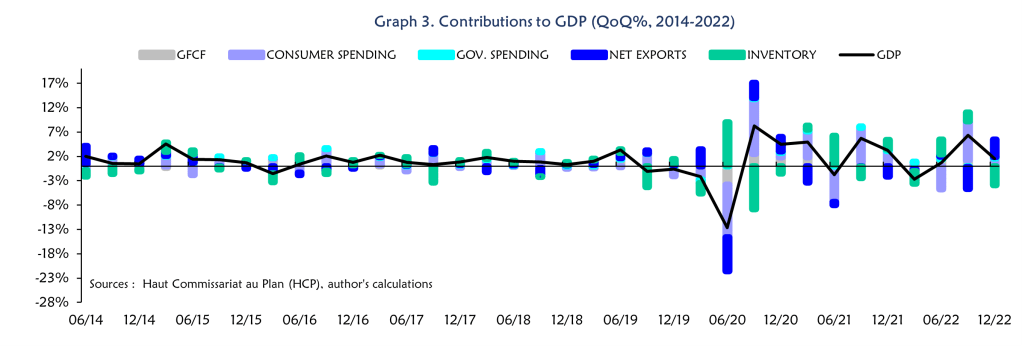

Forecasts and global cycle tend to weigh in favor of the previous view as Morocco is set to experience mild growth, in line with the stagflation tone dominating forecasts for world economies in 2023. The IMF expects global growth to fall to 2.9% in 2023, vs. 3.4% in 2022 while Morocco’s central bank forecasts a modest increase to 2.6% in 2023, up from the sluggish 1.2% in 2022. Granular data from the HCP shows clearly downward trends of both consumption (purple) and investment (grey) in Morocco’s GDP growth. Consumption’s reactions to closing and re-opening of the economy during the era of Covid lockdowns are patent, but since the return to normalcy, these shocks faded.

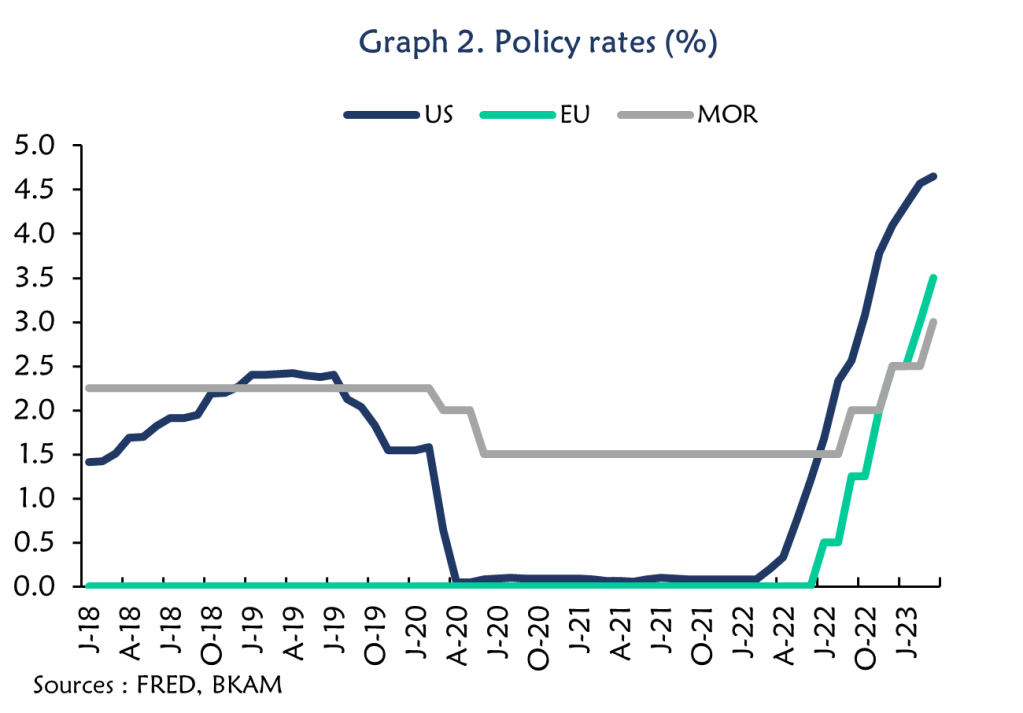

On another level, Bank Al Maghrib has been very conservative in its accomadative stance to support the Moroccan economy throughout the covid period, maintaining its policy rate at a timid 1.5% and safeguarding itself to venture in any QE operations, as many emerging market central banks experimented, sometimes successfully, during the period. Chances that current inflationary dynamics are moved by monetary factors are little to non existent.

These two points, the stagflation and the absence of monetary factors to inflation, have been the founding rationales of the critics of the central bank’s latest policy rate hike. Even the government expressed concerns over a monetary stance that tends to hamper growth dynamics, which will substantially harden the creation of one million additional jobs by 2026, the flagship electoral promise of the officiating majority.

One must nonetheless recall that Bank Al Maghrib monetary policy strategy is an exchange rate targeting strategy, not an inflation one, and that given global policy rates dynamic, the central bank is constrained to mimic the movement of the two crucial currencies for the floating peg of the dirham, the euro and the dollar.

With economic cycle and monetary dynamics excluded to explain the inflationary spike in Morocco, the remaining factor is the cost of production. This factor is two-fold : an imported and an endogenous component.

As previously stated, global dynamics in food and commodity markets are cooling down, going back to the levels of the pre-Russia-Ukraine conflict period. The local factor in turn points to a large set of structural issues and features of the Moroccan economy.

Deeply rooted aggravating factors :

When speaking about local factors aggravating the global inflation dynamic in Morocco, the matter simply and rapidly narrows down to competition policy issues and local markets structures. As a reminder of the essential interaction between competition, monetary policy and price controls, we would like to recall here France’s Competition Council’s head reaction to a Christine Lagarde’s statement on profit margins evolution in the euro area last March 22 : « If high corporate margins become entrenched, they will unduly sustain inflation. In such an environment, antitrust cannot substitute monetary policy, but it can usefully supplement it by fighting excess market power. »

Rightly so, excess market power and antitrust have been at the center of the debate lately in Morocco, especially in the energy and food sectors, the main drivers of Moroccan inflation.

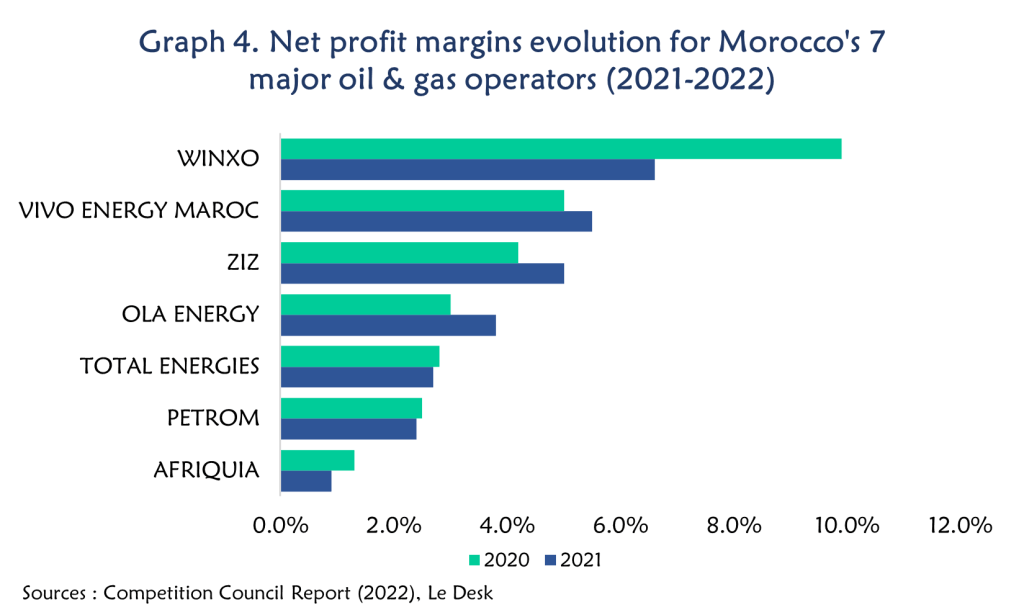

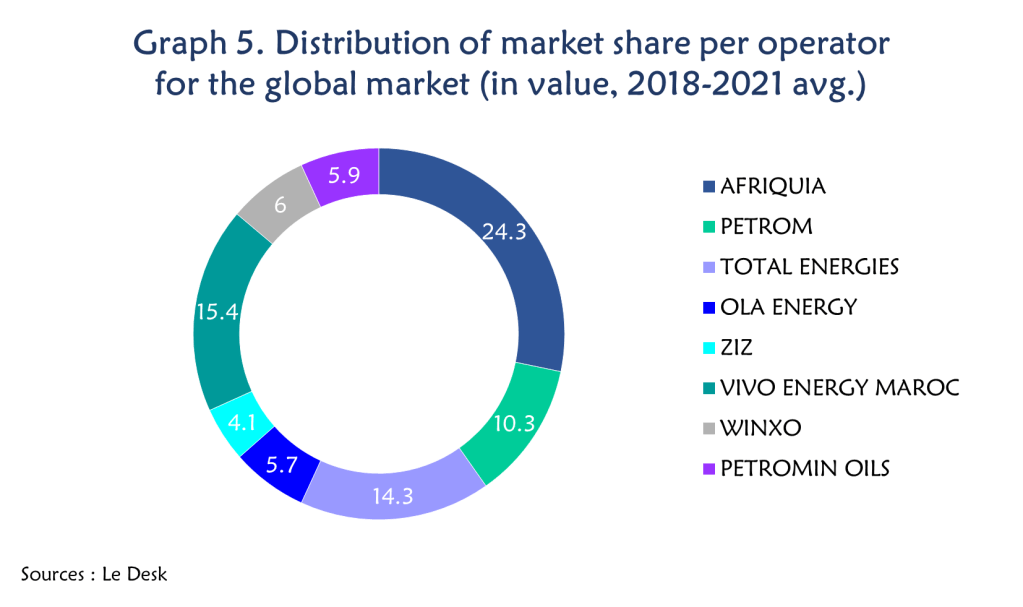

In the oil distribution sector, debate is ongoing since 2018 and the release of a parliamentary report on fuel prices. In 2020, an aborted antitrust sanction targeted major operators, while in 2022, the same antitrust body, with renewed leadership published a report underlined the neutralization of any form of price competition. From import to storage to gas stations, every level of the chain of value presents an oligopolistic structure with 7 major companies dominating the market. This quasi-monopole situation allows the companies to safeguard margins and market shares during high international oil prices phases, and further increase them during low phases.

Oil & gas aren’t the only inelastic products where failing market structures favour inflationary dynamics. It is frequent in the last months in Morocco that one food item goes through an erratic price increase and epitomizes public discontent about the evolution of price levels.

In fact, the commercialisation of food and agricultural products is mainly channelled through wholesale markets (33% of national production) that lacks efficiency and investment, are far from production regions, and obey to an archaic system selling rights that places enormous pricing powers on the hand of its owners. Those additional intermediaries are often the source of price surges, leveraging conjunctural factors as drought and bad crop, or the rise in seasonal demand, to outrageously expand their margins.

These structural features, coupled with cyclical impacts, leave the Moroccan citizen in a dire situation. In a Q3 2022 HCP household survey, 81 percent consider that their standard of living has deteriorated, and 87 percent expect an increase in unemployment going forward. Labour market is also taking a hit from this supply shocks as unemployment rate is steady, but participation rate is falling (from 50.8% in Q1 2022 to 48.1% in Q3 2022).

Reform opportunities to grow through the cycle :

Addressing these structural issues could provide Morocco with an opportunity to grow through the cycle and to reinforce its market share and brand power in global export markets.

In fact, if inflation is contained at reasonnable levels, the country could leverage the strong USD to further expand its industry exports thanks to an affordable MAD.

Morocco could also take profit of its good stance in the transition to a greener productive system, with opportunities in renewables and green hydrogen, plus its proximity to wealthy european markets downsizing shipping costs and overall production carbon emissions.

However, beforehand, Morocco must safeguard its macroeconomic and social stability to allow for such productive leaps, and this start with rapidly actionable reforms to neutralize pro-inflationary dynamics in essential sectors such as food and energy sectors.

Laisser un commentaire