This year (2020-2021), I really enjoyed my time as an assistant economist for the EEMEA region at Natixis. Since I left the position, many things are ongoing on the region, whether we talk about the heated relationships between Poland/Hungary and the EU, or the re-assessed growth prospects in the Middle East. The article provides a brief review of growth prospects and main macroeconomic and geopolitical themes across the region.

Few days ago, a webinar held by Ramona Moubarak and Gabriele De Leva of Fitch Ratings, on the Middle East Macroeconomic environment, allowed me to reconnect with the economic news of the area. In the article is a brief summary of the takeaways for those interested:

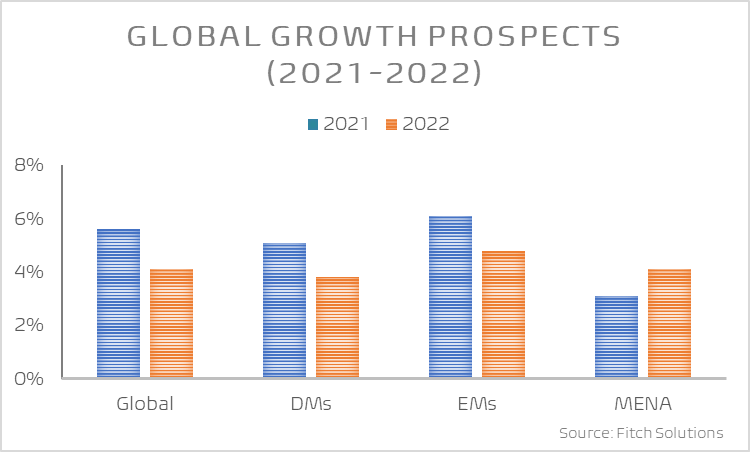

At the Global level:

Quite aligned with the IMF narrative, the world is on track for an uneven recovery. Yet, despite the unequal advancement of vaccine roll-out and different pandemic dynamics, EMs seem to lead the recovery, with China at the forefront. Global growth is expected to post at ~5.6% in 2021 and to slow to ~4.1% in 2022.

Ahead of the current adjustment phase to pent-up demand on international energy markets, oil prices should temper progressively as the market is structurally oversupplied. However, the oil barrel is expected to stay in the range of 80-90 USD in the near term.

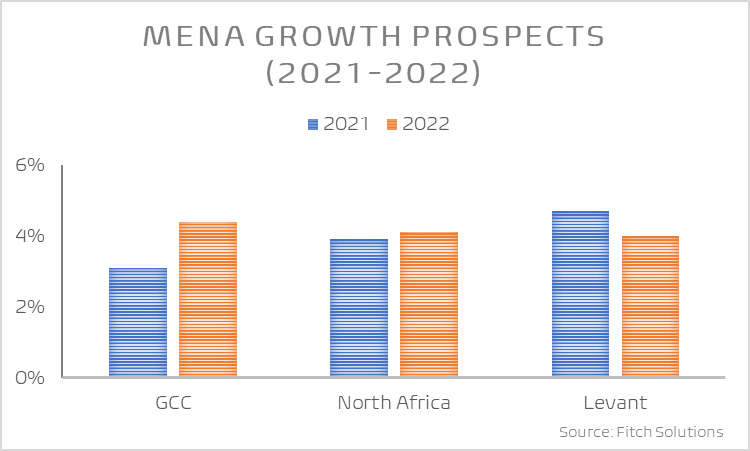

At the MENA level:

At 3.1% in 2021, the economic recovery in the MENA region is expected to be relatively weak, just at the level of the last 10-year trend growth. Divergence in vaccine roll-out and country specific drags on economies explain the sub-performance. Risk-wise, tourism is on the upside, with expected renewed flows of FX funds relieving the countries’ external positions, while country-specific structural and political risk features are tilting the outlook to the downside. 2022 growth for MENA should hover around 4.1% in 2022.

The Iran Nuclear Deal will concentrate the attention of investors and observers, as it will be the main source of risk and opportunity for the upcoming months in the region. Negotiations are expected to be tough, due to the high level of compromise that weigh on each part, yet both parties consider a deal as their best interest.

The GCC:

The monarchies group will outperform the MENA region growth, with 3.1% and 4.4% growth for 2021 and 2022, respectively. The GCC boasts a quick vaccine roll-out, with some spots such as Dubai considered as “normal life” microcosm amid a very pandemic-related restricted world. On the upside, international events of the like of Dubai Expo 2020 and FIFA WC 2022 in Qatar will drive conjunctural growth, while OPEP+ production cuts will dampen the hydrocarbon economy contributions to added value production.

North Africa:

Recovery should remain below the trend in 2021 and 2022 in North Africa, around 4%, with Egypt and Morocco on the lead.

Outlook seems bright in Egypt with improving vaccine roll-out, relaunch of tourism activity, and record high remittances fueling private consumption. Investment and net exports should also play favorably. Growth rate should be up to 5% and 5.5% for 2021/2022 and 2022/2023, respectively.

The picture is quite similar in Morocco, with and expected 5.3% growth in 2021. Fixed investment provided by the Covid-19 Mohammed VI Fund and the swift vaccine roll-out placed the country in favorable position for recovery. Soft fiscal tightening and accommodative monetary policy will allow this recovery to go on in the remaining months of 2021 and in 2022. Political risk however is high with heightened tension with Algeria.

Instability remains high in Tunisia and Libya, the Tunisian dinar going through a strong depreciation. Positive news might arise from the formation of a new government in Tunisia, a recent ceasefire, and the recovery of oil production in Libya.

The Levant:

GDP should grow 4.7% in the sub-region in 2021, mainly thanks to Israel’s contribution. Growth rate will slow to 4% in 2022. The outlook is however highly uneven, with countries in deep crisis like Lebanon, or with protracted structural deficiencies like Jordan and the issue of youth unemployment. Israel, at the top of the vaccination race, is taking advantage of a loose monetary policy and relative political consensus, as a budget was approved by parliament for the first time in 3 years.