As part of my Master Thesis assignment to complete the Masters in International Economics at Paris-Dauphine University, I chose to address the economic misfortunes of a country I am emotionally and personally attached to, Lebanon. Having known seldom periods of institutional stability, since 2019, Lebanon is in the midst of a severe economic, financial and social crisis. This article summarizes my work on the topic and provide a link to the ~30 pages thesis.

This is a series of extracts from my Master thesis. Full version is downloadable here.

The paper addresses four major points.

I. Dissecting the long-lasting macroeconomic imbalances that have led to the burst of the crisis:

« There are some striking figures that give a sense of the critical situations of Lebanon macroeconomic imbalances. As of July 2021, according to Reuters Eikon data, Lebanon’s outstanding foreign currency debt is up to USD 52.8 billion, that of Brazil is above USD 70 billion. In 2020, according to World Bank data, Brazilian GDP was 43 times larger than Lebanese GDP. In 2019, according to IMF data, Lebanon registered the 6th highest debt to GDP ratio of the 192 countries covered by the database, at 174.3%. That same year, the country also presents the 6th largest current account deficit, out of 193 countries for which data was available, standing at 26.5% of GDP. »

II. Explaining the reasons behind Lebanon’s apparent resistance to « macroeconomic gravity »:

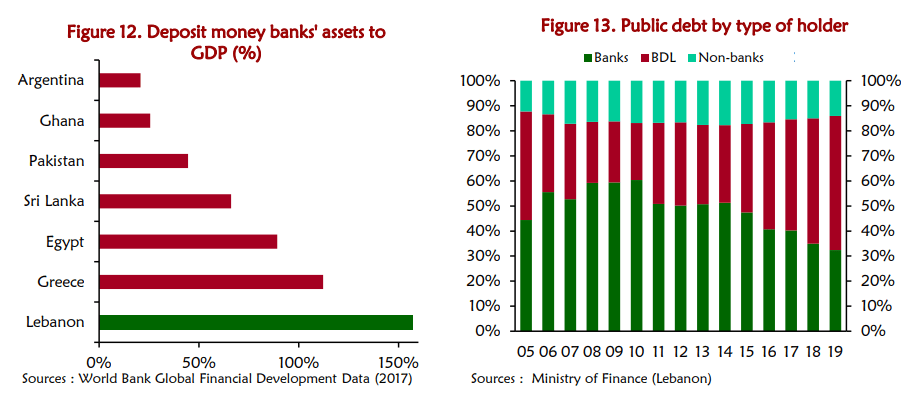

« By all standards, Lebanon has been running critical macroeconomic imbalances for over 15 years. How did the country kept financing its twin deficits and remained immune to any balance of payment or debt repayment crisis? The answer is three-fold: 1) A large banking sector committed to the sovereign solvency ; 2) Resilient remittance/deposit inflows ; 3) Strong international support. »

III. Analyzing the critics targeting the central bank peg policy and the so-called « financial engineering » operations:

« Until 2019, the BdL achieved its objective of exchange rate stability, keeping inflation at low levels. The period however was not free of headwinds. Lebanon experienced several shocks: the 2005 assassination of Prime Minister Rafiq Hariri, ongoing military conflict with Israel, the Syrian refugee crisis, and domestic political instability and governance weakness. The performance is real, but it came at incommensurate cost for the Lebanese future. »

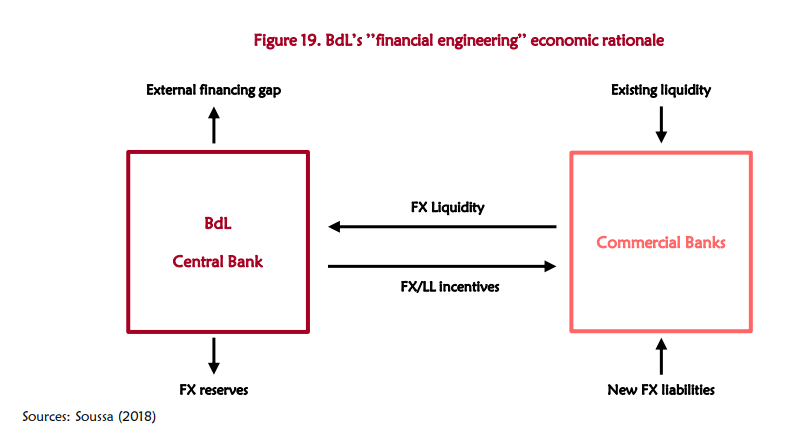

« Fearing the materialization of risks of collapse of the Lebanese financial system as its main sources of financing showed signed of depletion, the BdL introduced the so-called “financial engineering” operations in an ultimate attempt to attract FX funds, accentuating the features of a system some observers compared incidentally to a Ponzi scheme. »

IV. Exploring options for a crucial reform for a soft landing, the financial system restructuring, and taking a stance for a bail-in:

« As in any crisis, the main question is which party will bear the burden of adjustment. The restructuring plan presented above provide different answers to this question. Yet, looking at the wealth distribution in Lebanon, this paper takes a stance for a solution that will put banks’ shareholders and large depositors at the forefront of loss incurring parties. »